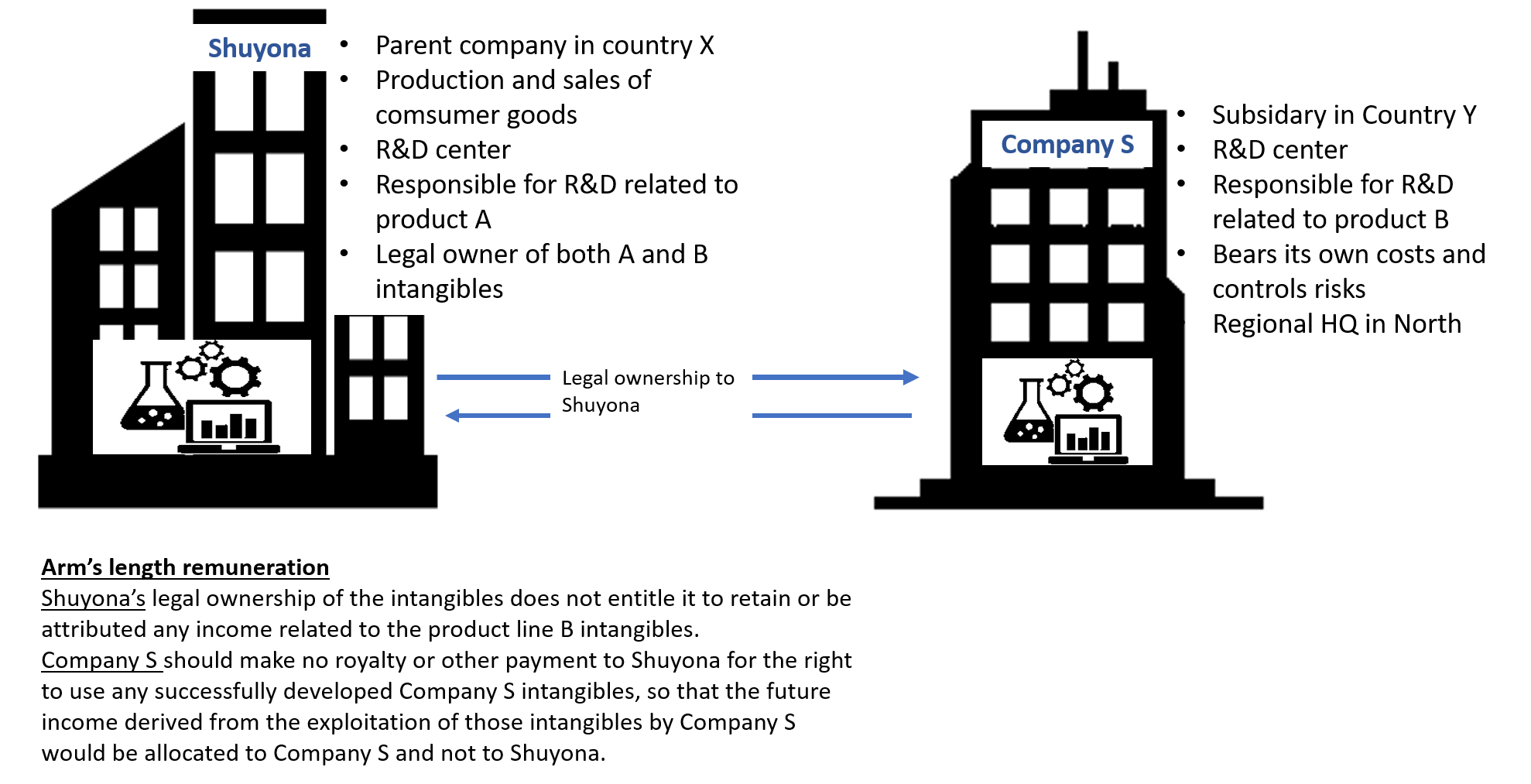

49. Shuyona is the parent company of an MNE group. Shuyona is organised in and operates exclusively in country X. The Shuyona group is involved in the production and sale of consumer goods. In order to maintain and, if possible, improve its market position, ongoing research is carried out by the Shuyona group to improve existing products and develop new products. The Shuyona group maintains two R&D centres, one operated by Shuyona in country X, and the other operated by Company S, a subsidiary of Shuyona, operating in country Y.

50. The Shuyona group sells two lines of products. All R&D with respect to product line A is conducted by Shuyona. All R&D with respect to product line B is conducted by the R&D centre operated by Company S. Company S also functions as the regional headquarters of the Shuyona group in North America and has global responsibility for the operation of the business relating to product line B. However, all patents developed through Company S research efforts are registered by Shuyona. Shuyona makes no or only a nominal payment to Company S in relation to the patentable inventions developed by the Company S R&D centre.

51. The Shuyona and Company S R&D centres operate autonomously. Each bears its own operating costs. Under the general policy direction of Shuyona senior management, the Company S R&D centre develops its own research programmes, establishes its own budgets, makes determinations as to when R&D projects should be terminated or modified, and hires its own R&D staff. The Company S R&D centre reports to the product line B management team in Company S, and does not report to the Shuyona R&D centre. Joint meetings between the Shuyona and Company S R&D teams are sometimes held to discuss research methods and common issues.

52. The transfer pricing analysis of this fact pattern would begin by recognising that Shuyona is the legal owner/registrant of intangibles developed by Company S. Unlike the situation in Example 14, however, Shuyona neither performs nor exercises control over the research functions carried out by Company S, including the important functions related to management, design, budgeting and funding that research. Accordingly, Shuyona’s legal ownership of the intangibles does not entitle it to retain or be attributed any income related to the product line B intangibles. Tax administrations could arrive at an appropriate transfer pricing outcome by recognising Shuyona’s legal ownership of the intangibles but by noting that, because of the contributions of Company S in the form of functions, assets, and risks, appropriate compensation to Company S for its contributions could be ensured by confirming that Company S should make no royalty or other payment to Shuyona for the right to use any successfully developed Company S intangibles, so that the future income derived from the exploitation of those intangibles by Company S would be allocated to Company S and not to Shuyona.

53. If Shuyona exploits the product line B intangibles by itself, Shuyona should provide appropriate compensation to Company S for its functions performed, assets used and risks assumed related to intangible development. In determining the appropriate level of compensation for Company S, the fact that Company S performs all of the important functions related to intangible development would likely make it inappropriate to treat Company S as the tested party in an R&D service arrangement.