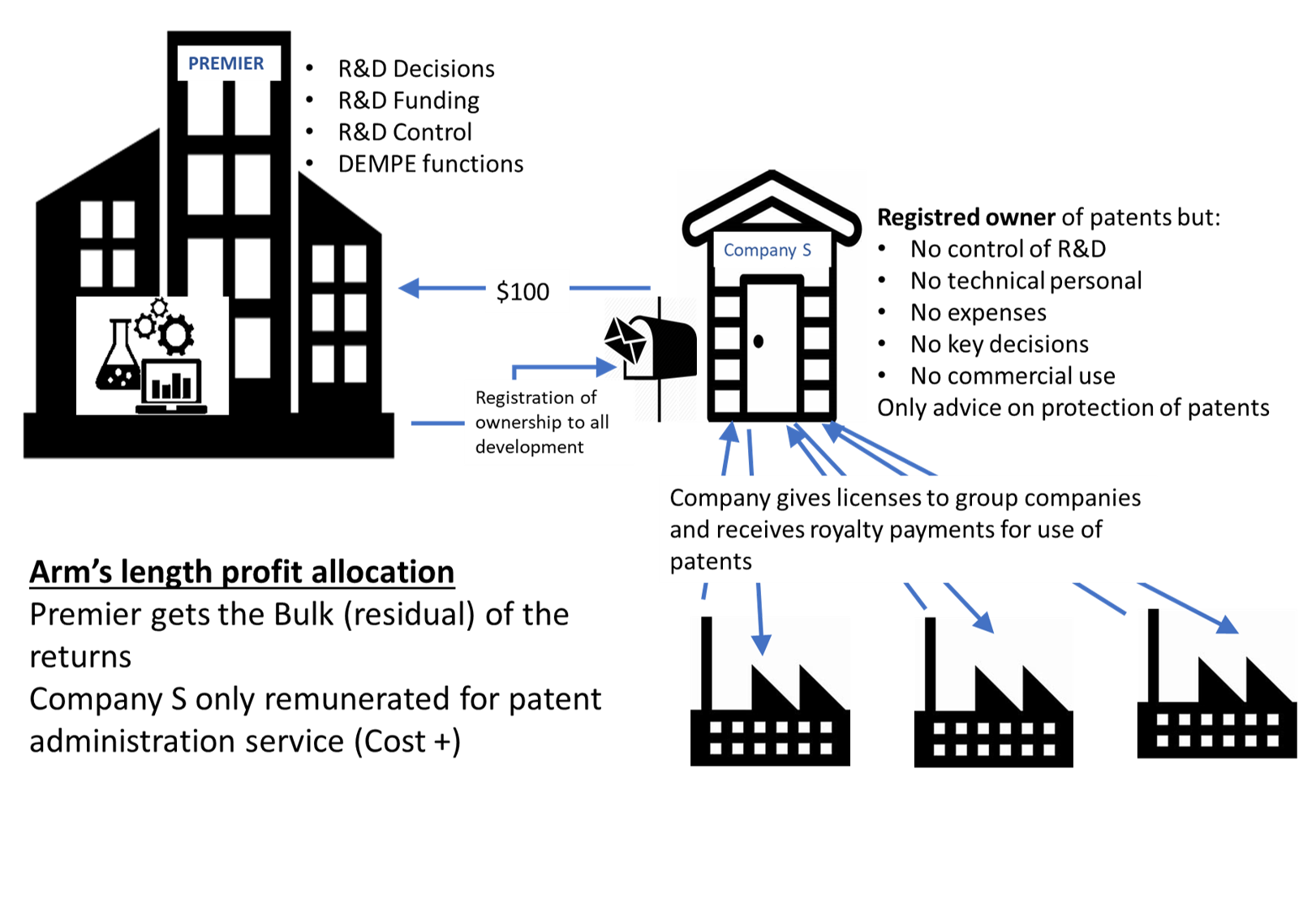

5. The facts related to the development and control of patentable inventions are the same as in Example 1. However, instead of granting a perpetual and exclusive licence of its patents back to Premiere, Company S, acting under the direction and control of Premiere, grants licences of its patents to associated and independent enterprises throughout the world in exchange for periodic royalties. For purposes of this example, it is assumed that the royalties paid to Company S by associated enterprises are all arm’s length.

6. Company S is the legal owner of the patents. However, its contributions to the development, enhancement, maintenance, protection, and exploitation of the patents are limited to the activities of its three employees in registering the patents and maintaining the patent registrations. The Company S employees do not control or participate in the licensing transactions involving the patents. Under these circumstances, Company S is only entitled to compensation for the functions it performs. Based on an analysis of the respective functions performed, assets used, and risks assumed by Premiere and Company S in developing, enhancing, maintaining, protecting, and exploiting the intangibles, Company S should not be entitled ultimately to retain or be attributed income from its licensing arrangements over and above the arm’s length compensation for its patent registration functions.

7. As in Example 1 the true nature of the arrangement is a patent administration service contract. The appropriate transfer pricing outcome can be achieved by ensuring that the amount paid by Company S in exchange for the assignments of patent rights appropriately reflects the respective functions performed, assets used, and risks assumed by Premiere and by Company S. Under such an approach, the compensation due to Premiere for the patentable inventions is equal to the licensing revenue of Company S less an appropriate return to the functions Company S performs.