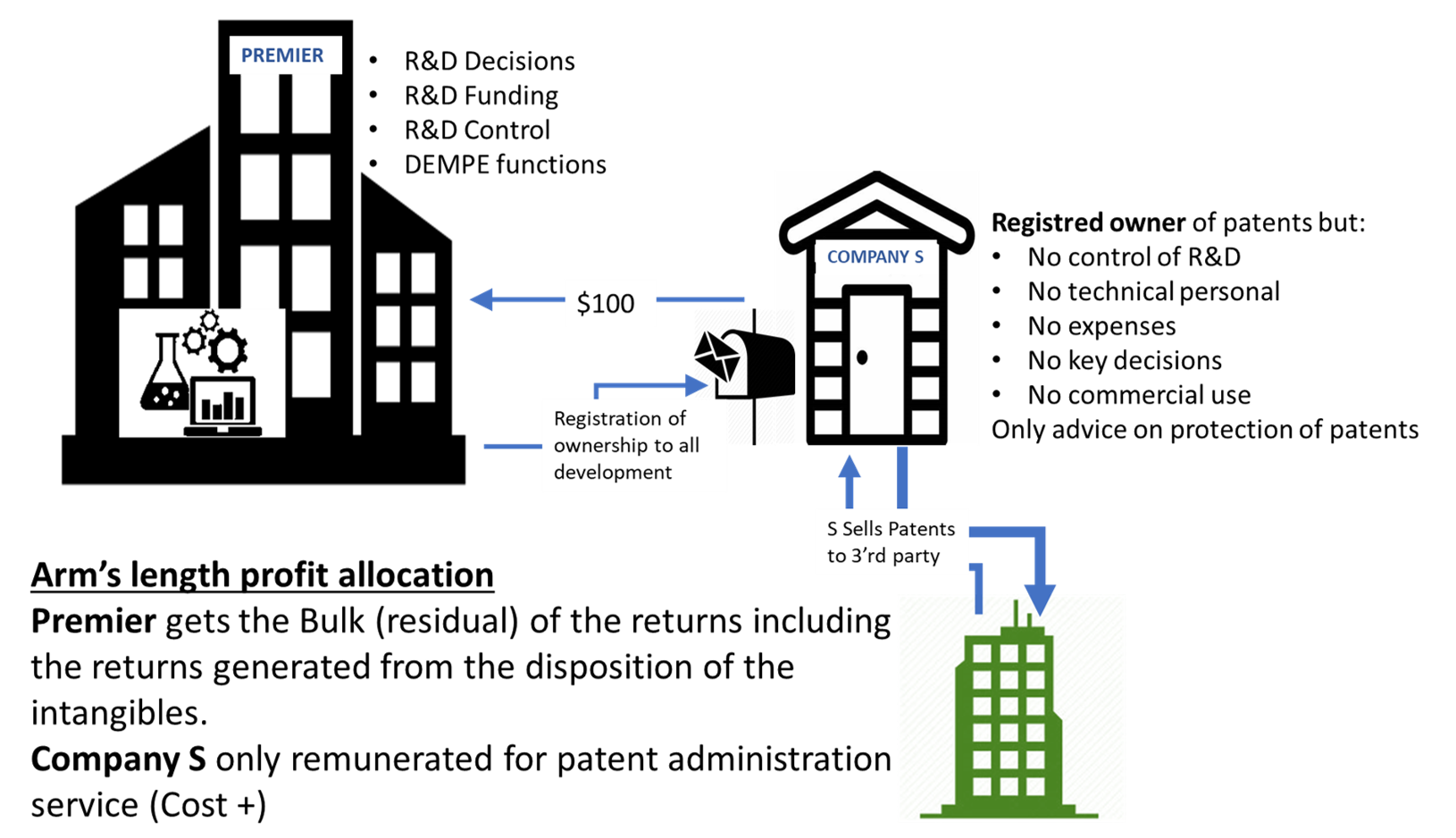

8. The facts are the same as in Example 2. However, after licensing the patents to associated and independent enterprises for a few years, Company S, again acting under the direction and control of Premiere, sells the patents to an independent enterprise at a price reflecting appreciation in the value of the patents during the period that Company S was the legal owner. The functions of Company S throughout the period it was the legal owner of the patents were limited to performing the patent registration functions described in Examples 1 and 2.

9. Under these circumstances, the income of Company S should be the same as in Example 2. It should be compensated for the registration functions it performs, but should not otherwise share in the returns derived from the exploitation of the intangibles, including the returns generated from the disposition of the intangibles.