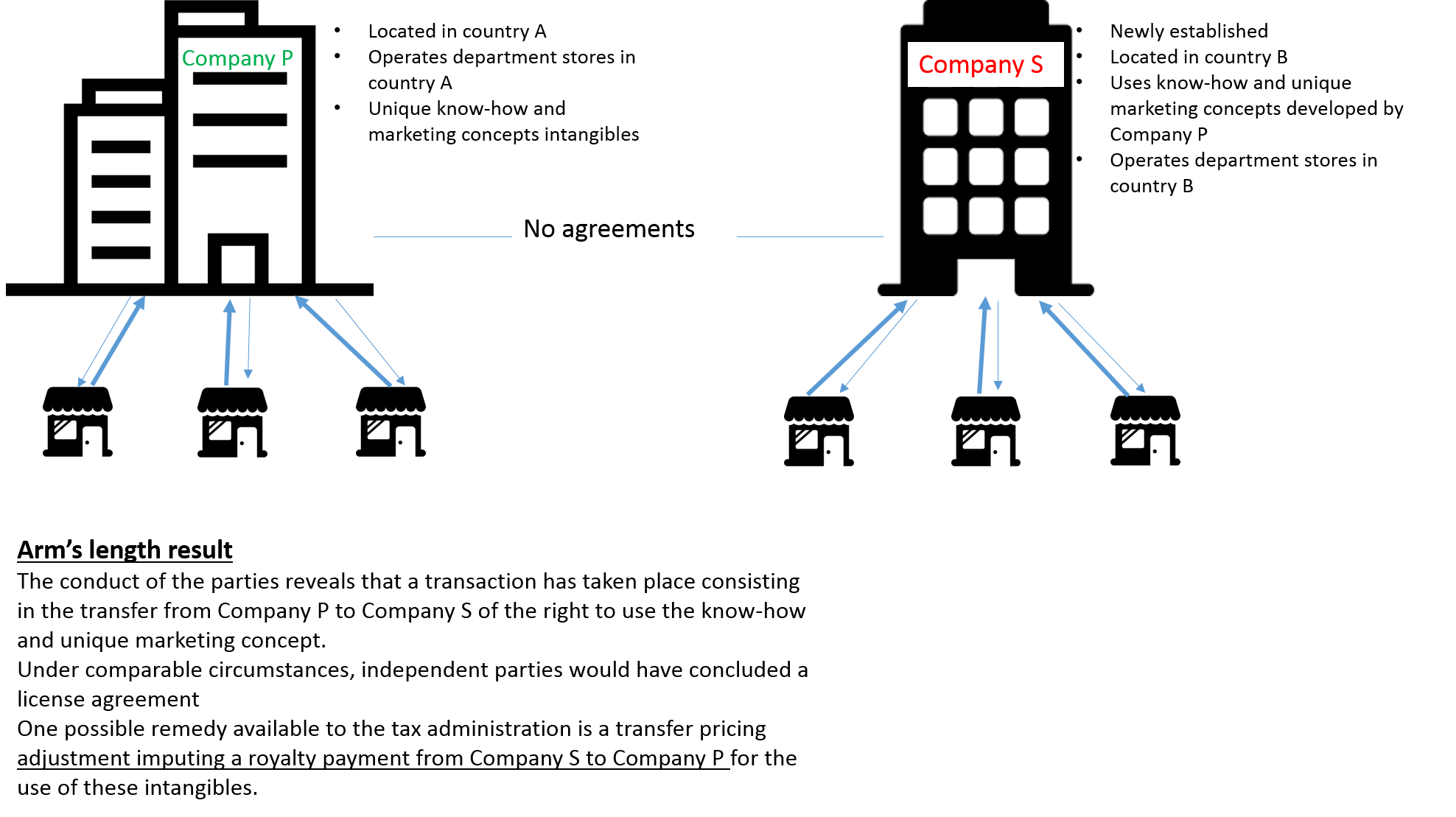

67. Company P, a resident of country A conducts a retailing business, operating several department stores in country A. Over the years, Company P has developed special know-how and a unique marketing concept for the operation of its department stores. It is assumed that the know-how and unique marketing concept constitute intangibles within the meaning of Section A of Chapter VI. After years of successfully conducting business in country A, Company P establishes a new subsidiary, Company S, in country B. Company S opens and operates new department stores in country B, obtaining profit margins substantially higher than those of otherwise comparable retailers in country B.

68. A detailed functional analysis reveals that Company S uses in its operations in country B, the same know-how and unique marketing concept as the ones used by Company P in its operations in country A. Under these circumstances, the conduct of the parties reveals that a transaction has taken place consisting in the transfer from Company P to Company S of the right to use the know-how and unique marketing concept. Under comparable circumstances, independent parties would have concluded a license agreement granting Company S the right to use in country B, the know-how and unique marketing concept developed by Company P. Accordingly, one possible remedy available to the tax administration is a transfer pricing adjustment imputing a royalty payment from Company S to Company P for the use of these intangibles.